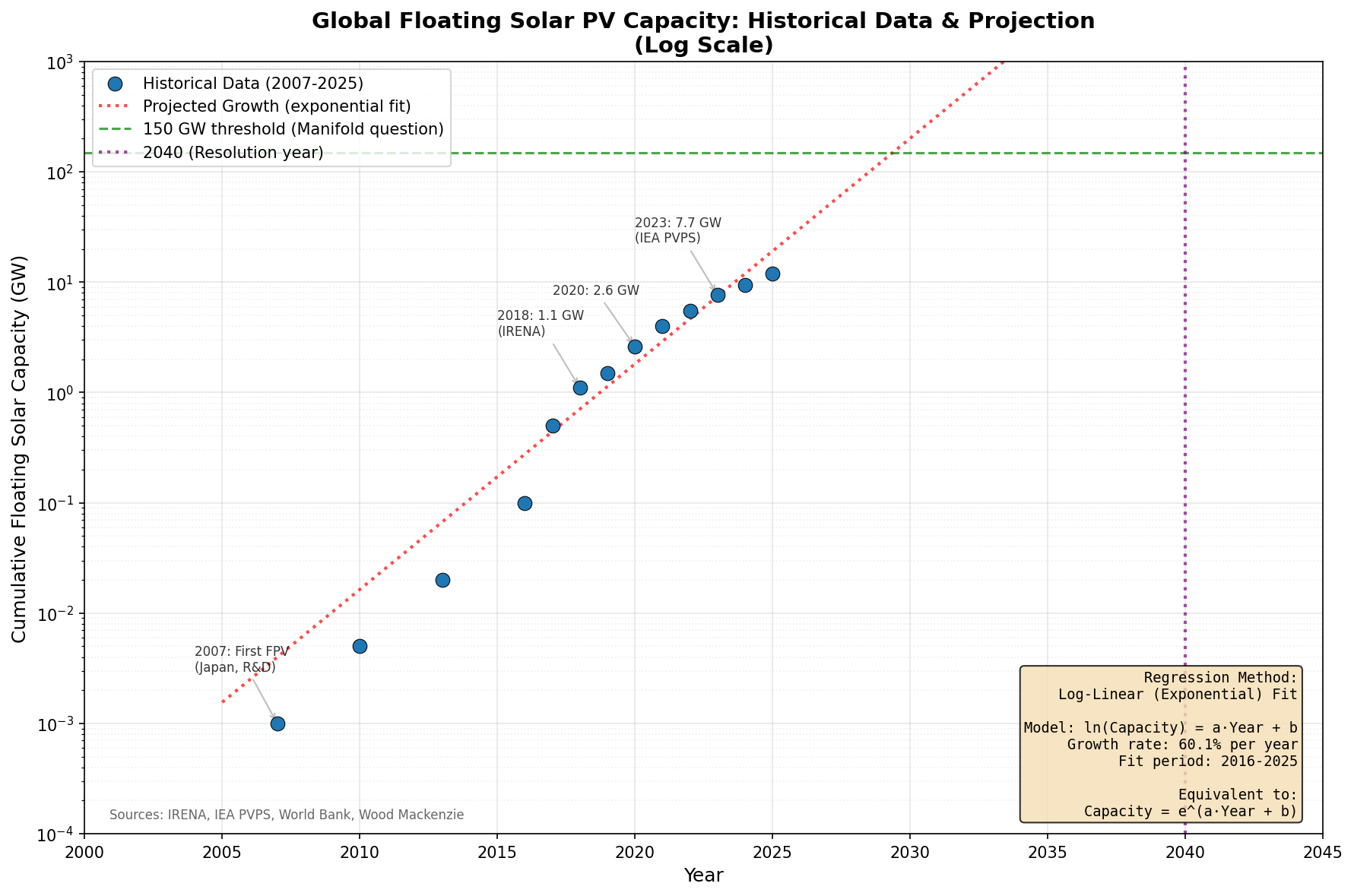

Resolves as YES if there is strong evidence that total cumulative installed floating solar photovoltaic (floating PV) capacity worldwide reaches at least 150 GWdc before January 1st 2040.

More detail and definitions:

What counts as “floating solar”?

PV modules mounted on floating structures on bodies of water: reservoirs, lakes, ponds, water‑filled quarries, artificial basins, and sheltered coastal or offshore sites.

Both freshwater and saltwater systems count.

Hybrid plants (e.g. hydro + floating PV) count, but only the PV nameplate capacity is relevant.

What capacity metric is used?

Capacity is measured in direct‑current gigawatts (GWdc), i.e. the PV nameplate rating (often also called GWp).

If a source only reports AC capacity, the resolver may convert to an approximate DC figure using a reasonable DC/AC ratio (for example, the ratio stated in the report or a standard value around 1.1–1.3).

Minor ambiguities or rounding in the conversion should be resolved in whichever direction seems most faithful to the underlying data; the intent is not to hinge the market on a 1–2 GW difference.

What counts as “installed”?

The capacity must be built, grid‑connected, and considered operational in the usual statistics.

Projects that are only announced, permitted, financed, or under construction do not count until they are reported as operational capacity.

Repowering or expansion of existing floating PV plants counts based on the resulting total operational PV capacity.

What counts as “worldwide cumulative capacity”?

Sum of all operational floating PV capacity across all countries at a given time.

This is typically reported by energy agencies, research organisations, or major analysts as a single global figure (e.g. “global floating PV capacity reached X GW”).

If global numbers are unavailable, the resolver may aggregate regional or country‑level figures from multiple reputable sources.

Sources and “strong evidence” for resolution

The market should be resolved using reputable, quantitative sources such as IEA PVPS reports, IRENA statistics, major analyst houses (e.g. BloombergNEF, S&P Global, Wood Mackenzie), peer‑reviewed meta‑analyses, or comparable global compilations.

“Strong evidence” means at least one high‑quality source explicitly gives a global floating PV capacity figure ≥ 150 GWdc, or several consistent sources imply this after reasonable conversion/aggregation.

The market can resolve early as soon as such evidence appears; it does not need to wait until 2040.

Edge cases

If there is disagreement across sources but all credible estimates are clearly below 150 GWdc, the market remains open.

If some sources put global floating solar slightly above 150 GWdc and others slightly below, the resolver should use whichever source appears most comprehensive and up‑to‑date; if that’s still ambiguous, they may take a simple average of the most credible estimates.

“Demonstration” systems that are not grid‑connected or are clearly labelled as temporary test rigs should be ignored unless they are included in the major global statistics being used.

The threshold 150 GWdc is chosen to be roughly my best‑guess median for global floating solar capacity by 2040: I see scenarios where the world falls well short of it and others where rapid deployment on reservoirs and coastal waters pushes well above it.

1,000

1,000