This is question #30 in the Astral Codex Ten 2023 Prediction Contest. The contest rules and full list of questions are available here. Market will resolve according to Scott Alexander’s judgment, as given through future posts on Astral Codex Ten.

1,000

1,000🏅 Top traders

| # | Trader | Total profit |

|---|---|---|

| 1 | Ṁ8,865 | |

| 2 | Ṁ697 | |

| 3 | Ṁ655 | |

| 4 | Ṁ389 | |

| 5 | Ṁ127 |

People are also trading

Scott Alexander clarified the question here:

> 1. Will US CPI inflation for 2023 average above 4%? Are you comparing CPI at the end of 2023 vs the end of 2022, the average CPI inflation across 12 months (CPI Jan 2023 vs CPI Jan 2022, CPI Feb 2023 vs CPI Feb 2022, etc.), or something else?

Let's say https://www.bls.gov/cpi/ will be the canonical site. If they don't update in time, it will be some other measure of year-on-year inflation.

@JonathanRay if so there's only been a cumulative 1.4% in the first 5 months of the period.

@JonathanRay 2.11% in the first 6 months if you exclude food and fuel: https://fred.stlouisfed.org/series/CPILFESL

@JonathanRay if you take out all the important things that cost more, there won’t be any apparent inflation

The mismatch between this market (at 18%) and Metaculus (at 50%) is wild to me https://www.metaculus.com/questions/14260/average-us-cpi-in-2023-over-4/

We have our first very large disagreement. 5-year TIPS are at 2.44% but somehow never got above about 3.5. Two-year treasuries pay 4.6%. Median forecast of the Philadelphia Fed Survey is 3.1%, and 3.0% core. The Fed has been rather wrong about this for a while now, and my average expectation here is going to be more like 3.5%, but we’ve had about seven months with relatively contained inflation numbers. Where does that put this percentage? Presumably somewhere in the middle between the two numbers. I’m going to buy M200 of YES here (and put M10 on the Yglesias market).

January CPI data just came out and was 0.5% MoM - i.e. 6% annualized. This matched the forecasts, and is higher than the December figure of 0.1%.

@jack Yes, and despite the current high reading, current forecasts are for a decline over 2023 to below 4% YoY. Latest median forecast from the Philadelphia Fed Survey of Professional Forecasters is 3.1%.

For core PCE, the median forecast is similar at 3.0%, and it's a different measure but I mention it because the survey asked forecasters for a probability distribution. The mean probability that forecasters assigned to PCE ≥ 4% was less than 10%. CPI is more variable, though, so one would expect a somewhat higher chance of CPI ≥ 4% than core PCE ≥ 4%.

@chrisjbillington I'd like to recall that average inflation is a different matter than 2023 inflation.

2023 inflation is whatever number is inflation for December.

@MP perhaps someone should ask Scott Alexander what he meant, but in a fairly standard mathematical use of terminology, YoY inflation in December is the same thing as average inflation over the year. IMHO it would be strange for the latter to mean something like "arithmetic mean of the 12 months' YoY inflation figures". In his 2022 prediction, Scott's wording for his inflation prediction was "Inflation for the year below five percent", for comparison.

@chrisjbillington Agree, I interpret this question as about inflation from the beginning of the year to the end of the year, i.e. YoY inflation at the end of December.

@mvdm Indeed. However the forecasters are expecting CPI to be lower than core PCE - 3.4% vs 3.7% for the year. So adjust downward a bit for the chances of CPI exceeding 4%.

Also note that the forecasters made their forecasts before the most recent CPI release, which surprised slightly to the downside by 0.14%. So further adjust downwards a smidge.

CPI disinflation has had a head-start looking at the year so far. Year-to-date annualised CPI is currently 3.99% and core PCE 4.85%. Core PCE for April isn't out yet, once it is released in a few days (such that comparison with CPI will be over the same months) the annualised year-to-date figure is expected to be about 4.55%.

So things are pointing to a somewhat lower CPI than core PCE.

Also of relevance is the lagging nature of housing costs in inflation measures, which might create short-term upward pressure on inflation stats, though the cooling (in the Denver area where I'm casually looking) RE prices have been going down, so we can expect some lagged benefit later this year to offset:

Jan inflation report due out Tuesday. Cleveland Fed has an inflation nowcast and is projecting January MoM to be 0.64% which would be almost 8% annualized! However, here is their recent track record when predicting a couple of days before the release:

MO FCST ACT

Jul 0.27% -0.02%

Aug 0.06% 0.12%

Sep 0.32% 0.39%

Oct 0.76% 0.44%

Nov 0.46% 0.10%

Dec 0.12% -0.08%

The cumulative annualized prediction for last 6 months is ~4.0% vs actual of 1.9%, so their model has been overshooting by >100%. For fun, I generated 6 random numbers between -0.1% and 0.5% to make my own "forecast" and came up with a cumulative annualized inflation of 1.5%, with my forecast being closer to actual in 3 of 6 months. Not a great look, Cleveland Fed!

https://www.clevelandfed.org/indicators-and-data/inflation-nowcasting

In case you're wondering, I calculated a bonus random number to serve as my January CPI inflation prediction and got 0.3%. You're welcome.

@KCS Al Quinn has posted a couple of comments explaining his thinking, so either this is (play) money on the ground or Al Quinn is the sucker...you decide!

Come o people--this is mispriced. CPI has averaged below a 2% annual rate over the last 6 months; month-over-month numbers will need to rise from the recent average of ~0.15% to >0.3% for all of 2023 to hit 4%. The year-over-year inflation number that is more prominently reported takes trailing 12 months and obscures the more recent trend indicating a drastic moderation.

@AlQuinn But also:

Starting with January 2023 data, the BLS plans to update weights annually for the Consumer Price Index based on a single calendar year of data, using consumer expenditure data from 2021. This reflects a change from prior practice of updating weights biennially using two years of expenditure data.

And

@MattCWilson Do you predict the change in weighting will be that significant in terms of the reported number? Looks like a relatively minor change and I don't expect year-to-year change in how category weightings are set to be decisive for this question, though that is an additional variable to consider (wonder if they will report 2023 Jan in comparison to legacy method to see if any big differences).

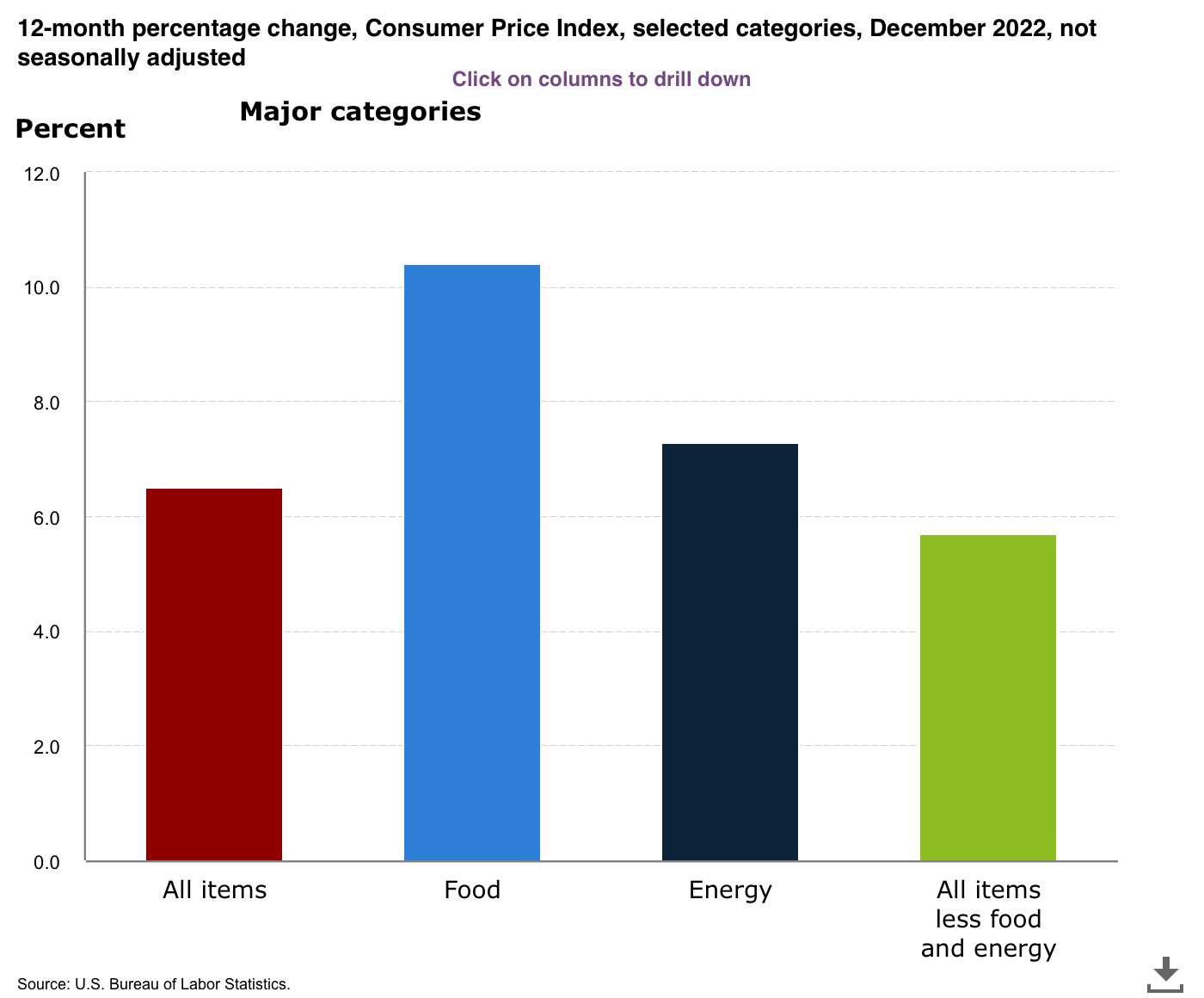

Second, I already pointed out the issue with the December 2022 data: that is full year and the vast majority of that inflation happened in the first half:

2022 1st half annualized inflation: 10.9%

2022 2nd half annualized inflation: 1.8%

2022 full year inflation: 6.4%

@AlQuinn I’m not sure. 2021 was the middle of the pandemic - if the last weights were using 2019-2020 (or 2018-2019? I’m not sure when they last reweighted) that is a very different economic condition to baseline from.

Just observing reasons that might explain the reasoning.