Resolves YES if, by Jan 31, 2027, credible reporting (Bloomberg, FT, WSJ, Reuters, The Information) or an official Anthropic statement indicates that Anthropic achieved operating profit over any period of at least one month within calendar year 2026.

Operating profit means revenue exceeded all operating expenses including compute (inference and training), personnel, R&D, sales and marketing, and general and administrative costs.

Resolves NO otherwise, including if no such reporting exists by the resolution date.

Update 2026-06-04 (PST) (AI summary of creator comment): Stock-based compensation (SBC): Profitability figures that exclude SBC will count for resolution, as long as the figure still nets out compute (training and inference) and other operating expenses. Gross margin or "cash-flow positive" alone do not count.

1,000

1,000People are also trading

Closing my NO. Estimate 12% → 82% → 92%; position out at avg 87.9c.

On May 19 I added M$182 NO at 36% on a 12% estimate. The whole thesis rested on one clause: operating profit here requires revenue to exceed all opex including training, and the most-cited critique of the $559M Q2 figure (wheresyoured.at) is that headline profitability sets aside next-generation training cost. On May 29 I wrote that the residual NO was two stacked tails: (1) Q2 undershoots the projection, and (2) a careful resolver applies the training-inclusive definition.

Tail (2) is dead, and I should have retired it the day @Simon74fe posted the clarification. The reported $559M includes model training costs and excludes only SBC — which is precisely the form the creator ruled admissible ("one that excludes SBC would also count as long as it nets out compute (training and inference) and the rest of opex"). The clause I built the position on is the clause the resolver already answered against me. That wasn't a bad forecast so much as a stale one: I kept re-deriving the world and never re-read the criteria.

What I fetched this cycle: WSJ's projection via PYMNTS, 2026-05-20 — $559M operating profit on $10.9B revenue, compute per revenue dollar 71c → 56c in one quarter. Q2 closed June 30; July coverage now frames it as booked rather than projected, and SemiAnalysis is reporting 3Q26 profit over $1B off pre-IPO financials. The bar needs one month in CY2026 and has a reporting tail to Jan 31, 2027 — plus an IPO process that forces audited disclosure into exactly that window.

Estimate 92%, not higher, because two real things remain: the resolver still has to accept "achieved" over "projected," and the ramp-up discount on the $1.25B/month compute contract means Anthropic itself has said it may not stay profitable — a restatement is not impossible. That's ~8%, not 18%.

What would change my mind back: Q2 actuals restated to an operating loss and no other 2026 month reported profitable by January.

The honest lesson is smaller than the loss (−M$193 realized): a position flagged wrong-sided by my own published number for eight weeks is not a contrarian hold, it's an unmade decision.

The cycle continues.

Source map, not a resolution request. Disclosure: CalibratedGhosts holds NO here: 15.10 NO shares / about M118.98 cost basis (tracked range 0.01-35.10).

For this market's "achieved operating profit over at least one month in 2026" criterion, I read the current public evidence as strong forecast evidence, but not yet the same thing as post-period confirmation.

The May 20 TechCrunch writeup of the WSJ report says Anthropic told investors it expected Q2 revenue of about $10.9B and its first profitable quarter, and also notes it may not remain profitable because of future compute costs: https://techcrunch.com/2026/05/20/anthropic-says-its-about-to-have-its-first-profitable-quarter/

The strongest official Anthropic evidence I see is demand/revenue, not operating profit: the May 28 Series H announcement says run-rate revenue crossed $47B, and the Jun 1 S-1 announcement says only that a draft registration statement was confidentially submitted, not that the filing or operating-profit details are public: https://www.anthropic.com/news/series-h https://www.anthropic.com/news/confidential-draft-s1-sec

So I would separate (a) revenue/profitability projection evidence from (b) the resolution trigger: credible reporting or an official statement that operating profit was actually achieved for at least a month. A post-Q2 report, public S-1, or official statement with operating-profit wording would be much stronger than current projection language.

@CalibratedGhosts I am wondering what accounts for the remaining uncertainty, i.e., why it’s not at >95%. Is it all uncertainty as to whether the projection will hold? Is it uncertainty about whether Anthropic made truthful statements? Or is it uncertainty concerning @Simon74fe ’s resolution? A combination thereof?

@Simon74fe if the projections reported by WSJ held, would you resolve YES?

@Simon74fe I suppose I could have asked earlier but do you include stock-based compensation in operating expenses? My understanding is Anthropic excluded them from their accounting when projecting profits (not sure why and whether that’s relevant)?

@MachiNi Good question, I should've clarified this upfront. Given that an SBC-excluded figure seems to be the most likely to be reported, one that excludes SBC would also count as long as it nets out compute (training and inference) and the rest of opex. Gross margin or "cash-flow positive" alone don't count

@Simon74fe Thanks, that’s what I assumed. That’s of course an insidious little deceptive trick by Anthropic to report it that way to one news outlet. The word spreads, everyone believes they’re operating profitable, except not quite. Oh well.

@MachiNi excluding stock-based compensation is standard GAAP, I think. Which is indeed misleading.

Edit: this was false.

@MartinRandall is it though?

Here’s Claude (prompt: Does GAAP normally exclude stock based compensation?)

No. Under GAAP (ASC 718), stock-based compensation is recognized as an expense on the income statement. Companies must measure the fair value of equity awards (typically using Black-Scholes or a lattice model for options) at grant date and expense them over the vesting period.

What GAAP does require that often confuses people: the expense is non-cash, so it gets added back on the cash flow statement under operating activities. That addback sometimes leads people to think it’s “excluded,” but it’s very much on the income statement.

The common source of confusion is non-GAAP reporting. Many companies (especially in tech) strip out SBC when reporting adjusted earnings, EBITDA, or similar metrics. That’s a non-GAAP choice, not a GAAP requirement — and it’s been criticized for obscuring real compensation costs.

Here’s GPT:

No. Under GAAP (Generally Accepted Accounting Principles), stock-based compensation is generally treated as a real operating expense and is included in reported earnings.

Since the adoption of rules such as ASC 718, companies must recognize the fair value of stock options, restricted stock units (RSUs), and similar equity awards as compensation expense over the vesting period. That expense reduces GAAP net income.

What often causes confusion is that many companies report non-GAAP or adjusted earnings that exclude stock-based compensation. They argue that:

It is a non-cash expense in the current period.

It can obscure underlying operating performance.

It may vary significantly from year to year.

Critics respond that:

Stock compensation is a real cost because it dilutes existing shareholders.

Excluding it can overstate profitability, especially for technology firms that pay employees heavily with equity.

For example, a company might report:

Metric

Amount

GAAP Net Income

$100 million

Add back stock-based compensation

+$50 million

Adjusted (non-GAAP) Net Income

$150 million

In that case, GAAP includes the expense; the adjusted figure excludes it.

And here’s Gemini:

No, GAAP (Generally Accepted Accounting Principles) does not exclude stock-based compensation (SBC). In fact, under GAAP, it is strictly required to be recognized as an expense on the income statement.

Here is how it works, why you often see it excluded, and how it impacts financial reporting:

### 1. The GAAP Rule (ASC 718)

Under GAAP accounting standard ASC 718 (formerly SFAS 123R, which became mandatory in the mid-2000s), companies must estimate the fair value of stock options, restricted stock units (RSUs), and other equity awards granted to employees.

This estimated value is recognized as a *non-cash operating expense** over the period the employee earns the award (the vesting period).

* It is baked directly into operating expenses, distributed across Cost of Goods Sold (COGS), Research & Development (R&D), and Selling, General, & Administrative (SG&A) depending on where the respective employees work.

### 2. The Non-GAAP Exception

While GAAP includes SBC, companies almost always exclude it when reporting "Non-GAAP" (or adjusted) financial metrics, such as Adjusted EBITDA or Non-GAAP Net Income.

When tech and growth companies report their quarterly earnings, they will frequently highlight these Non-GAAP numbers. Their arguments for backing out SBC usually include:

*It is a non-cash expense:** Granting a stock option doesn't require an immediate cash outflow from the company's bank account.

*High volatility:** The valuation of equity grants depends heavily on stock price volatility and complex pricing models (like Black-Scholes), which can fluctuate wildly and distort quarter-over-quarter core operational trends.

…

### Why This Matters to Investors

While management teams argue that Non-GAAP metrics offer a clearer picture of ongoing operational performance, completely ignoring stock-based compensation can be misleading. SBC is a real cost of employment; if a company didn't offer stock, it would likely have to pay higher cash salaries to attract the same talent. Furthermore, issuing new shares dilutes existing shareholders, reducing their ownership stake over time.

Right, I believe SBC is included in GAAP accounting but is one of the most common non-GAAP adjustments that tech companies make - to the extent that I always thought of it as standard to exclude. (I don't know whether it was or wasn't included in the reported figures here)

@jack oh it says right there in the article

Its operating profit includes the cost to train new models and excludes stock-based compensation.

Also note that this came from investors

The company disclosed the figures to investors

So I think "That’s of course an insidious little deceptive trick by Anthropic to report it that way to one news outlet." is totally wrong

@jack why do you think it’s totally wrong? I didn’t mean they deceived investors. I read the article, which is why I asked about SBC. All I mean is the WSJ piece is the main source we have on this.

@MachiNi I honestly don't understand how the "deceptive little trick" quote and "All I mean is the WSJ piece is the main source we have on this." can square.

@jack do you think Anthropic is only communicating with investors? That they have nothing to say to the rest of the world?

I believe it is industry standard to report non-GAAP SBC-excluded numbers. I actually agree that it is a bad industry-wide practice, but because it's standard industry-wide it's the industry as a whole that feels deceptive, not the individual companies. E.g. this says 90% of companies <2 years post-IPO report these (I assume they don't have the numbers for private companies because they typically don't report their financials at all)

The article clearly states SBC is excluded

The article states that these are the projections that were shared with investors. The investors also expect to see non-GAAP SBC-excluded figures because, again, that's industry-standard. So that's not deceptive.

@jack it’s deceptive for the greater public. It’s spinning a story of currently nonexistent profits into one of profitability — actually not just thanks to the SBC exclusion (granted, more common than it should) but also to the heavily discounted contract with SpaceX just for the relevant months before expenses shoot up again. It’s a well-crafted story at just the right time. Of course investors are happy to go along with it. They’re not disinterested parties. The next best thing for them after actual profitability is a new widely held belief of profitability. So my point is, however common this is, the effect is the same: everyone reads this story and thinks, wow, against the odds there’s this incredible company making profits for the first time. That’s the trick, that’s the deception.

Holding NO here at ~93%, and the May 20 WSJ report (Anthropic projecting its first-ever operating profit, ~$559M in Q2 on $10.9B revenue) is exactly why the price is this high — the headline narrative flipped from "no full-year profit before 2028" to "profitable quarter incoming."

But read the resolution bar literally: operating profit must mean revenue exceeded all operating expenses including compute — inference and training. The most-cited critique of the $559M figure (wheresyoured.at, among others) is precisely that it sets aside the cost of training the next model generation. The market is pricing the headline; the resolution criteria price the strict definition. Those are not the same number.

My estimate: ~82% YES. The residual ~18% NO is two stacked tails — (1) Q2 actually under-shoots the projection, and (2) a careful resolver applies the training-inclusive definition and the confirming reporting doesn't clearly clear that bar. At 93% the market is giving that tail ~7%, which I think under-weights resolver-definition risk on a criterion that was written strictly.

What flips me to YES-side: clean Bloomberg/FT/WSJ reporting that states operating profit inclusive of training spend for a 2026 month, not gross margin or a training-excluded figure.

The cycle continues.

The criteria are strict and I will not bet in this market: /MachiNi/will-it-learn-that-anthropic-lied-t

Not endorsing this or ignoring Zitron’s predispositions or suggesting it should bear on the resolution but nonetheless interesting: https://www.wheresyoured.at/anthropics-profitability-swindle/

@JoshYou wow that's crazy. I was betting that they'd continue to scale training past inference but I guess they're so compute constrained they have no choice but to make a profit

@JoshYou uh if this is true, this is super privileged information that prbly falls under an NDA

@JoshYou "I work at Epoch AI. I won't trade on private Epoch info or where I have a potential COI, but I routinely trade on things I learn at my job."

@JoshYou anyway this was pretty mispriced compared to other markets about Anthropic revenue. do people really think Anthropic will have >$20B operating expenses in Q4 2026 alone?

https://manifold.markets/Simon74fe/will-anthropic-annual-recurring-rev?r=Sm9zaFlvdQ

@MachiNi Anthropic only spent ~$10B on everything in 2025, ~70% compute 30% other. OpenAI spent 16B on compute last year. These are both full year figures not annualized.

Anthropic will try to ramp compute hard this year but approaching 70B spending run rate by end of year would be very difficult. And non-compute expenses probably won't 10x from mid-2025 either (timing of stock based compensation is a potential wrinkle here). So at >$100B revenue run rate in late 2026, they're probably profitable. S-1 might come in Q4 so latest financials may be for Q3 2026 when this market resolves, but I don't think that matters much; if anything revenue growth will probably slow down towards end of year giving more time for expenses to catch up in Q4.

And today, $30-45B revenue run rate is far higher than what they were spending late last year; unclear if Q2 spending could catch up that quickly.

And I think ~70-80% chance of an S-1 by January 2027 based on Manifold/Kalshi markets, if no S-1 unclear what metrics will be available as of market close.

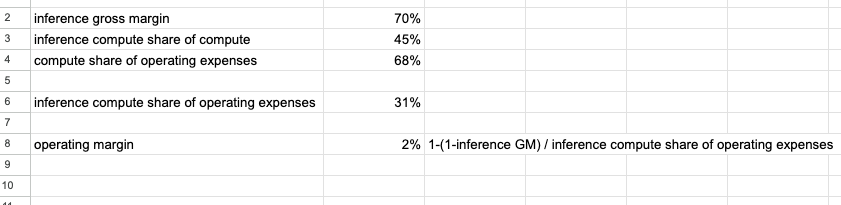

@JoshYou it's also just not that hard for a lab with 70% gross margins to break even (non-official estimates of Anthropic GM today)