Context:

Currently, it looks like in raw intelligence

Gemini 3.1 Pro (Google) > GPT-5.4 (OpenAI) > Claude Opus 4.6 (Anthropic)

yet in terms of market share / usability

Anthropic (Claude Code) > OpenAI (Codex) > Google (Antigravity / Gemini CLI)

this suggests there’s an inherent tradeoff between effort put into improving the underlying model and the integration with the harness

where Google (and OpenAI) focus more on tasks like multimodality (image / video gen) long context, math, chess and hope the other capabilities come down stream of that increased intelligence

Anthropic is much more focused on coding / SWE and the tools (MCP / Skills / Claude Code) to enable training data specific to the domain they’re hill climbing on, they’ve also made Claude much more humanlike in behavior with things like soul documents and Claude seems to have by far the best non-reasoning models as well and generally more jailbreak resistant (Google is by far worst at that)

Context:

Recent interview with OpenAI Chief Scientist:

https://youtu.be/vK1qEF3a3WM?si=Mc9hOdHrHjO9msII

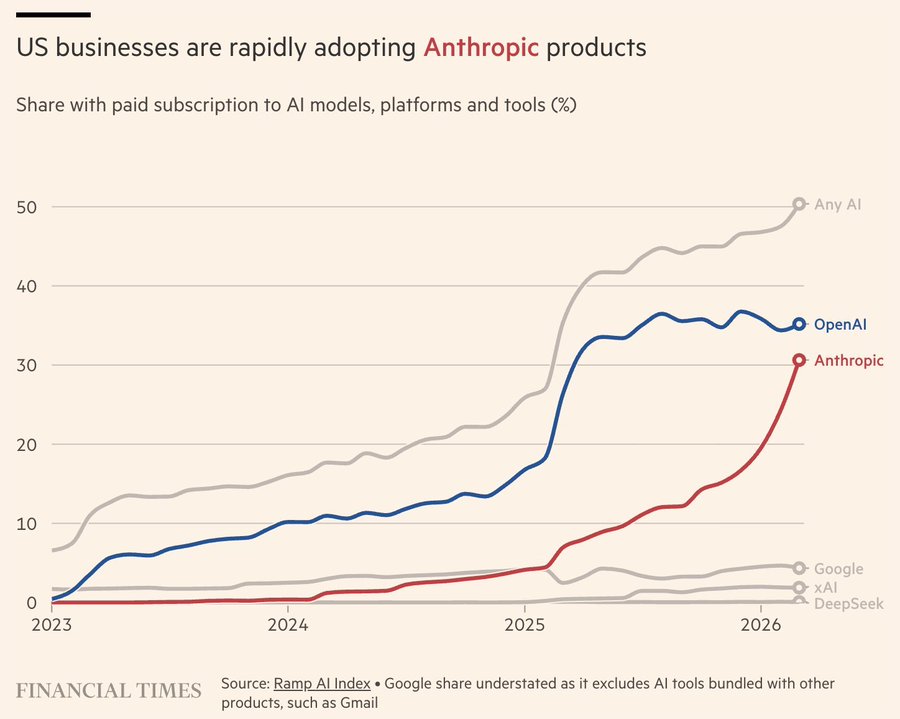

Anthropic:

https://x.com/rohanpaul_ai/status/2043008591242891315?s=20

Gaining market share rapidly amid DoD drama, reportedly increased from 9B ARR run rate last year to 30B just 3 months into 2026 (https://finance.yahoo.com/news/anthropic-tops-30-billion-run-221045473.html )

Already poised to overtake OpenAI in valuation (918B vs 868B on ventuals)

https://manifold.markets/EricNeyman/when-will-anthropic-surpass-openai

Mythos seems like a sign Anthropic might have taken the lead once and for all at least in coding, but too early to tell whether the lead in coding translates to other domains they’re clearly behind in (e.g. math, world models)

Google:

Google is definitely focusing more on “Personal Intelligence” and their models historical suck at agentic coding due to a tendency to attend to all the context at once which makes it require hacks to be able to attempt to use tool calls for long running tasks

Relevant benchmarks

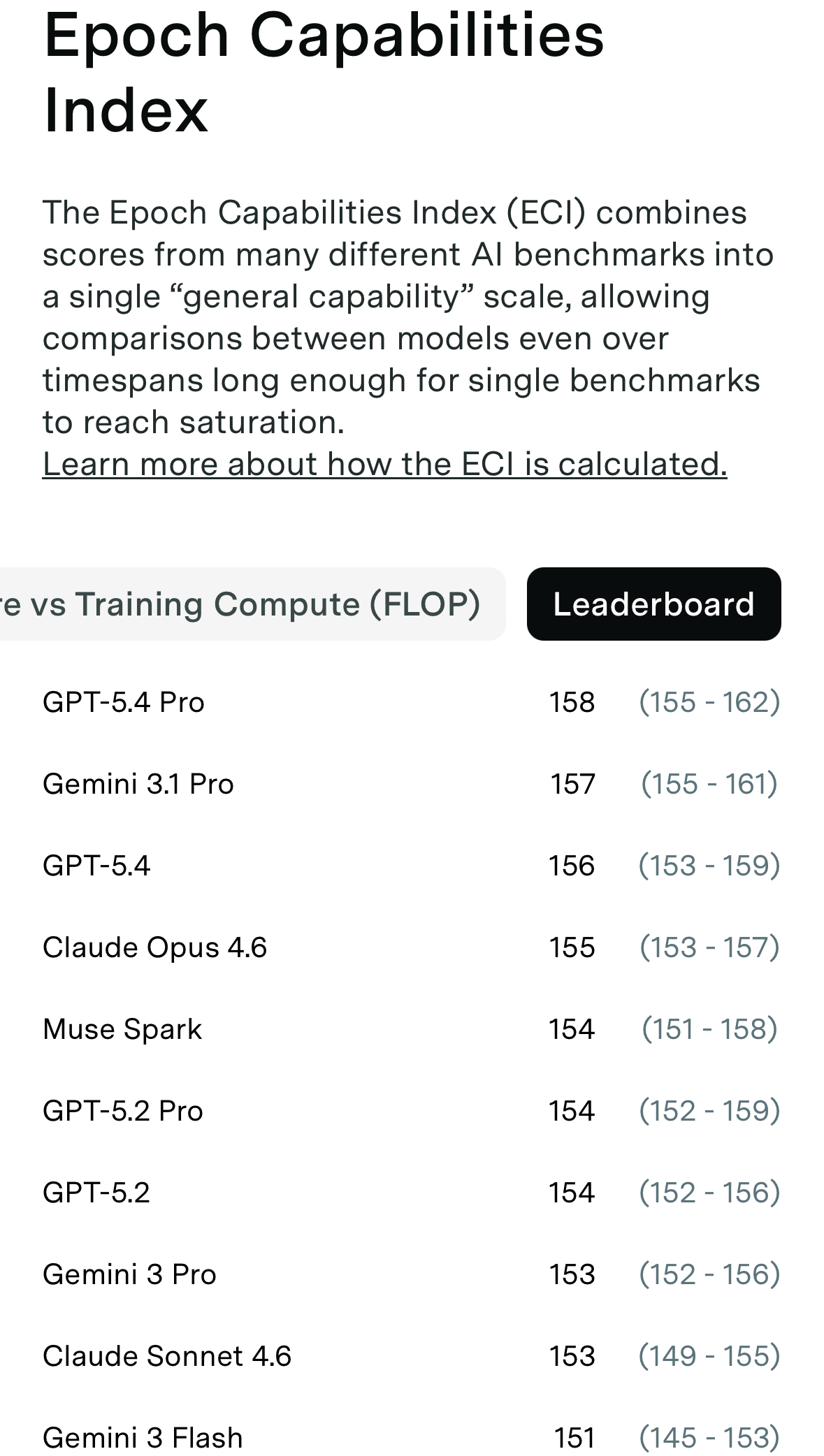

ECI (and all the specific benchmarks going into that, namely seems like Frontier math and chess are what make OpenAI and Google ahead of Anthropic) https://epoch.ai/eci/?view=graph&tab=release-date

OpenAI: 156/158

Google: 157

Anthropic: 155

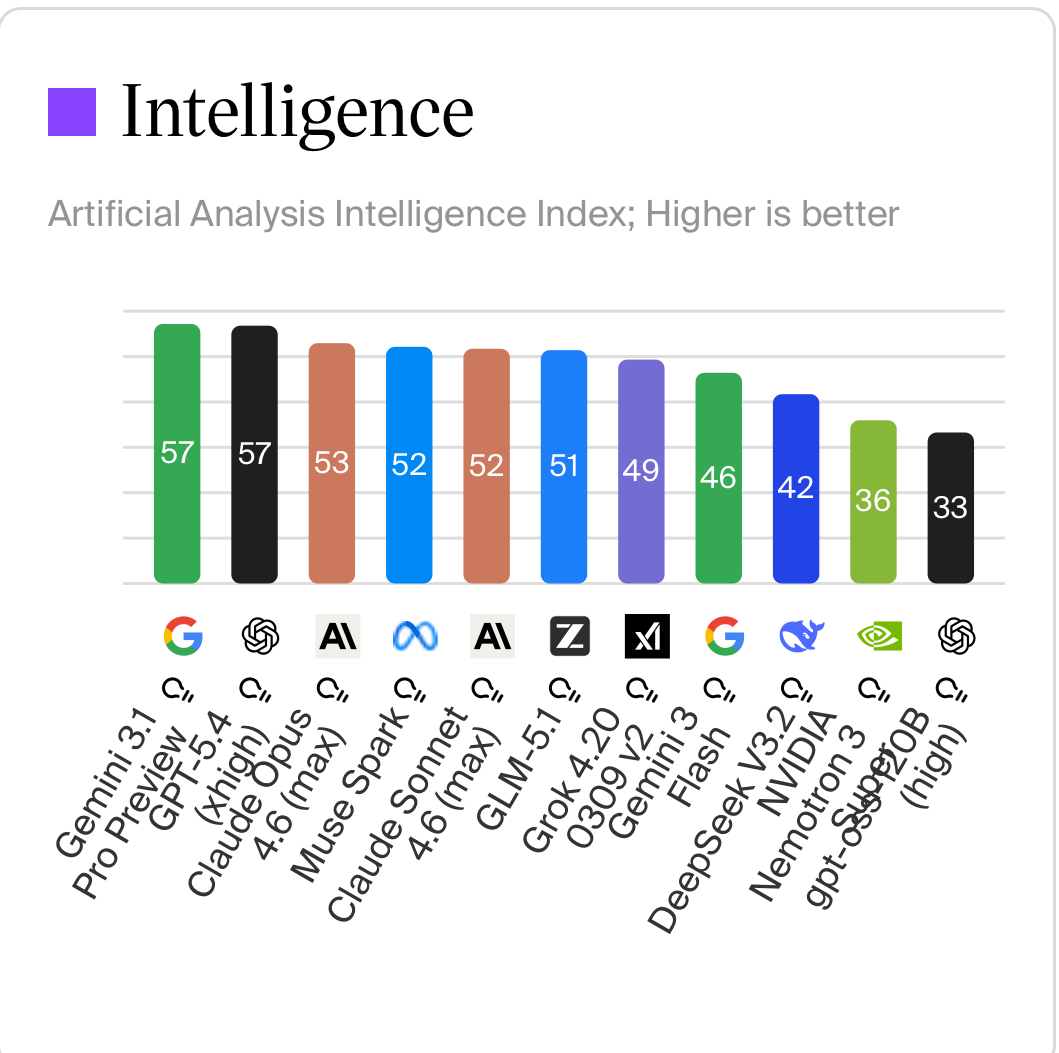

AA Intelligence (another aggregator focusing on one shot tasks which where Google and OpenAI seem to perform better): https://artificialanalysis.ai

Google: 57

OpenAI: 57

Anthropic: 53

Benchmarks that favor Anthropic:

Versions of SWE bench that focus on long running / code churn:

can’t seem to find the exact link - https://www.lesswrong.com/posts/nAMhbz5sfpcynjPP5/swe-bench-pro-is-even-worse, I saw in some recent video

maybe it was evoclaw: https://arxiv.org/pdf/2603.13428

or actually SWE-CI was probably what I was looking for: https://arxiv.org/pdf/2603.03823

Ok enough background

will resolve in a year with possibility to extend to another year if it’s unclear (kind of like now)

Yes = the trend is proven correct where Anthropic seems to pull ahead due to sole focus on code / enterprise consumer whereas OpenAI and Google’s focus on general intelligence / research / frontier causes them to lose market share to Anthropic who achieve some kind of special sauce focusing on their ecosystem. Essentially yes = in the next 1-2 years Anthropic seems to have some moat (kinda like Apples walled garden ecosystem vs Android) even though benchmarks seem to say other models are more intelligent (hopefully the inverse Goodharts doesn’t apply e.g. the benchmarks are made to match the subjective opinion that Anthropic models feel much better)

No = everything I said above is largely irrelevant and there’s no such divergence

N/A / unclear is if we’re still in some state of relative ambiguity like we are now and no such conclusion can be made

To recap the main motivation for this market is that I initially was interested in whether OpenAI willfail / collapse / have its bubble pop based on recent news like their 1.4T investment commitment being lowered to 600B e.g. if / when they fall out of the top 3 but I don’t think that’s very likely short term particularly with their lead in math research, so this market is more focused on the divergence between the “Intelligence” and how that translates into market share / revenue in the next 1-2 years

1,000

1,000